The Governmental Accounting Standards Board (GASB) Statement Number 103, Financial Reporting Model Improvements (GASB 103), is officially in effect, which means state and local governments need to update significant portions of your financial statement to comply. The changes within GASB 103 are intended to improve the effectiveness of the financial reporting model by making financial statements more understandable and useful for decision-making – not only for financial professionals, but also for a broader range of users who rely on this information to evaluate a government’s accountability and performance.

Tips for Navigating the Changes in GASB 103

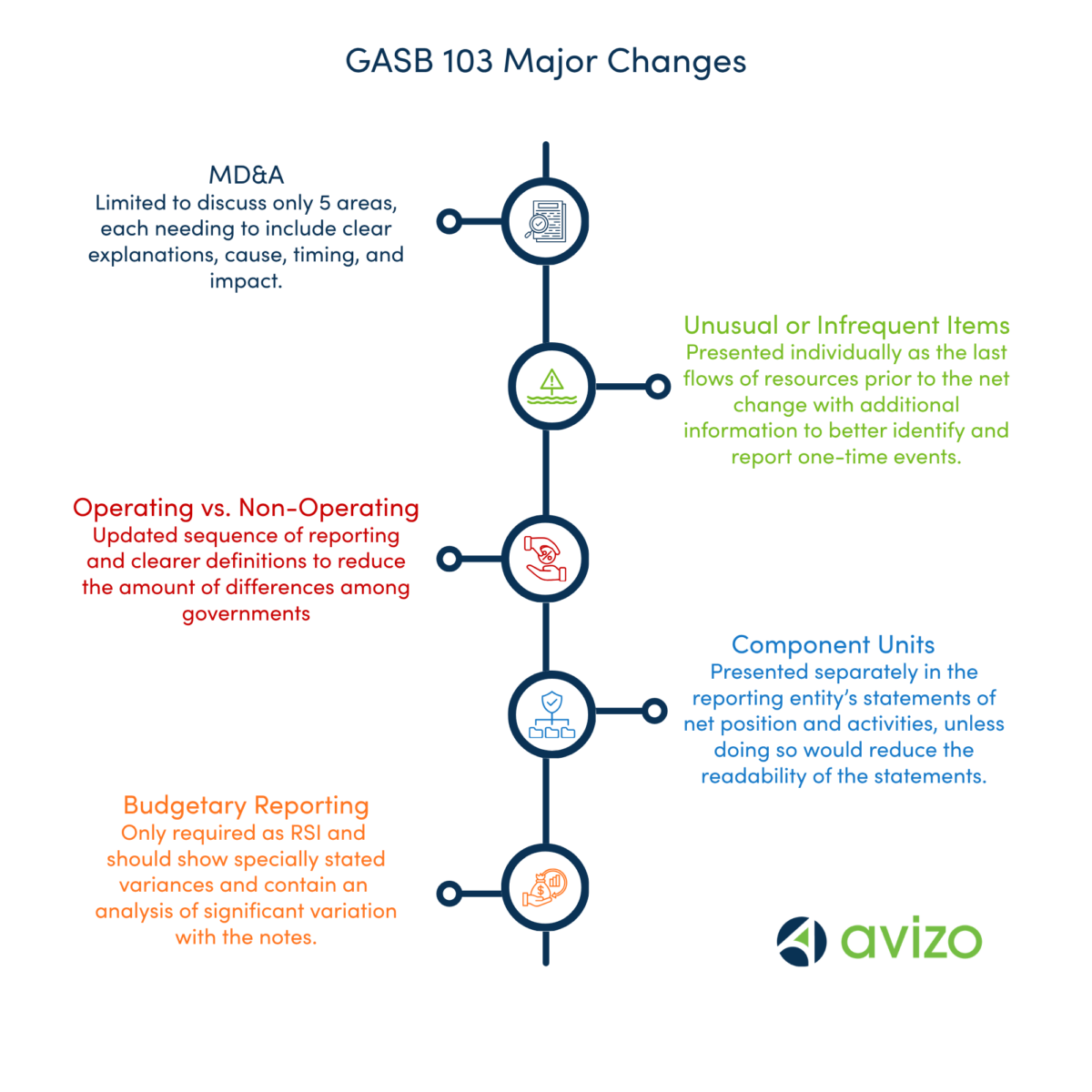

The key areas of the financial reporting model that are impacted include the following: Management’s Discussion and Analysis (MD&A), Unusual or Infrequent Items, Operating vs. Non-Operating – Proprietary Fund Statements, Component Units, and Budgetary Reporting. Our assurance team will take care of the majority of these changes for the entities we work with to ensure compliance, but if you are not a current client, continue reading or request our full guide to GASB 103.

MD&A

Our tip for the Management’s Discussion & Analysis narrative is to stop following a template-style narrative and really delve into specifics with commonly understandable language. The MD&A section is now limited to five content areas listed below, preventing the inclusion of extraneous topics. Each of these areas needs to be detailed with clear explanation of the reason and impact of all changes:

- Overview of the Financial Statements

- Condensed Financial Summary

- Detailed Analyses

- Significant Capital Asset and Long-Term Financing Activity

- Currently Known Facts, Decisions, or Conditions.

Information not related to these five topics should be omitted from the MD&A going forward. Instead, focus on these topics and explain the cause, timing, and impact of the changes on current operations to provide additional context for the financial statement users’ analysis. This information will be presented as Required Supplementary Information (RSI).

Unusual or Infrequent Items

The update for “unusual or infrequent items” requires re-organization instead of having major content changes. Items within this section were previously labeled as “extraordinary” or “special” and they are now grouped under “unusual or infrequent.” You should present them in the following way:

- List them individually;

- Present as the last presented flows of resources, prior to the net change;

- Include both inflows and outflows of resources;

- Include a note to disclose whether an unusual or infrequent item is within the control of management.

Operating vs. Non-Operating

This section contains several changes. First, operating and Non-Operating items have been redefined to reduce the amount of differences among governments and to clarify the results from operations for proprietary funds. You can read more about these definitions on our original blog explaining the GASB 103 changes.

In addition to the recategorization of what is operating and nonoperating, there is an updated format to the Statement of Revenues, Expenses, and Changes in Net Position (SRECNP) that contains a new subtotal for noncapital subsidies. We recommend that you review the new definitions, particularly for nonoperating items – any activity that does not fit within the new nonoperating categories is now considered operating, so you may have to reclassify from previous financial statements.

Component Units

The components unit is another section that has been restructured so that each major discretely presented component unit is presented separately within the primary statements of net position. You will not be allowed to aggregate multiple significant component units into a single column. Detailed information should be included instead of listed within the notes.

Budgetary Reporting

Lastly, if your entity presents annual budget-to-actual comparisons, you can no longer present the budgetary comparisons as basic financial statements. Instead, these comparisons must now be shown as Required Supplementary Information and must include explanations of significant variations.

Changes in GASB 103

Overall, going forward, financial statements need to be focused on specific information but provide detailed explanations of the information. Avizo’s assurance team will take care of the majority of these changes for the entities we work with to ensure compliance. We will work directly with you to re-define needed changes, such as of operating and non-operating items. If you have any questions regarding these changes and how they will affect your financial statements in 2026 and 2027, please do not hesitate to reach out.

Kirsten Owens, CPA

A Manager on our assurance team, Kirsten maintains expertise to provide auditing services with a specialization in Avizo’s governmental and construction-based niches. She is one of the primary leads on our in-field audits and completes training for all members of the firm before they visit clients offices.