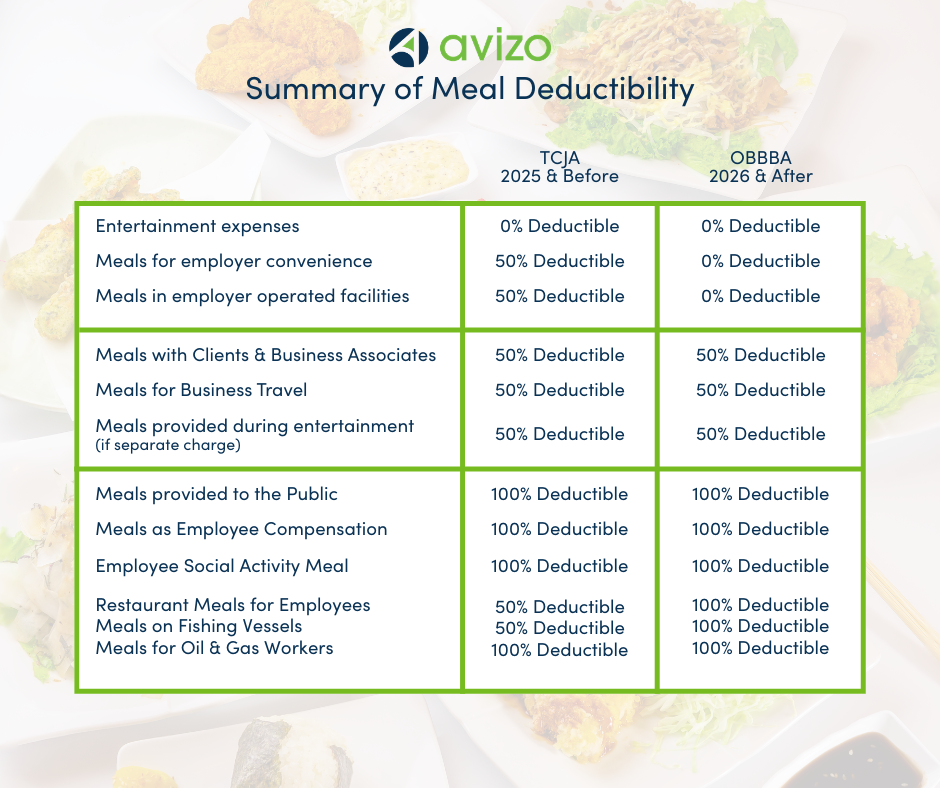

The One Big Beautiful Bill Act (OBBBA) brought a major change to meal expenses, snacks or drinks provided by an employer for the employer’s convenience. After January 1, 2026, these costs are now non-deductible. Most of the other meal expenses remain unchanged, but if your organization has traditionally provided meals and snacks for employees, this can have a big impact on your 2026 taxes.

0% Business Meal Expenses in 2026

Starting in 2026, businesses who provide lunches and snacks to employees will no longer be able to deduct the costs of doing so. Exceptions exist for meals provided by restaurants for their employees, meals on fishing vessels, and meals sold to the public at full-price in employer-operated cafeterias. Review the list below for meal expenses that cannot be deducted in 2026.

- On-Site Cafeteria and Meals (NEW): Meals served or other food provided in breakrooms or through employer-operated kitchens, and subsidized cafeterias, when the meals are not taxed as employee income are no longer deductible.

- Food and Snacks (NEW): on premises de minimis food or beverages like snacks, coffee, and soft drinks offered to employees for free or a reduced cost.

- Entertainment-Related: Meals considered to be entertainment-related continue to be nondeductible, unless the meal is separate from the entertainment.

- Personal-Related: Meals that cannot be sufficiently documented as being related to business activities remain nondeductible.

50% Business Meal Expenses Deduction in 2026

There are no changes to the tax rules that fall into the 50% deductible category, but it important to maintain all documentation required by the IRS in order to deduct these. Please see the last section of this blog for guidelines.

- Business Travel Meals: Travel expenses, including meals and lodging, are deductible if they are incurred while away from home in the pursuit of a trade or business. These expenses must be reasonable and necessary.

- Business Meals with Clients or Prospects: If an employee is present and the meal is not part of an entertainment activity, you can continue to deduct 50% of the meal cost.

100% Deductible Meals

Likewise, there are no changes to meals that can be entirely deducted in 2026 and these include the following:

- General Public: Food and beverages made available primarily to the general public, such as complimentary coffee and snacks in a showroom or customer waiting area, remain fully deductible, provided they are not primarily for employees. Likewise, meals offered to the public for marketing or promotional purposes are 100% deductible.

- Treated as Compensation: If meal expenses are treated as compensation to the recipient and included in wages, the employer can deduct it as wages.

- Employee Social Activities: Meals provided to your employees as part of a social or recreational event (company picnic, holiday party) are still 100% deductible.

- Certain Industries: Exceptions exist for meals provided by restaurants for their employees, meals on fishing vessels, and meals for those working in oil and gas.

Maintain Documentation for Meal Expenses

The IRS To qualify for any deduction, each meal should meet the following criteria:

- Be considered ordinary and necessary expenses paid or incurred in carrying on a trade or business.

- Not be lavish or extravagant under the circumstances.

- Involve the taxpayer or an employee being present when the food or beverages are provided.

- Be properly substantiated – maintain documentation that includes the receipts with the amount, date, and place; include your notation of the business purpose and business relationship of attendees.

Be sure that all meal expenses are well-documented according to these guidelines to maintain compliance with IRS regulations. If you have any questions, our team is here to help.

Chris VanArsdale

Chris is a Manager in our tax department with over 10 years of experience. His specialties include international, trust and estate, and business tax filings.