Accounting Changes and Error Corrections

GASB 100

Compensated Absence

GASB 101

Public Private Partnerships and Availability Payment Arrangements

GASB 94

Subscription-Based Information Technology Arrangements

GASB 96

{kind=link}

The Annual Comprehensive Financial Report

GASB 98

Omnibus 2022

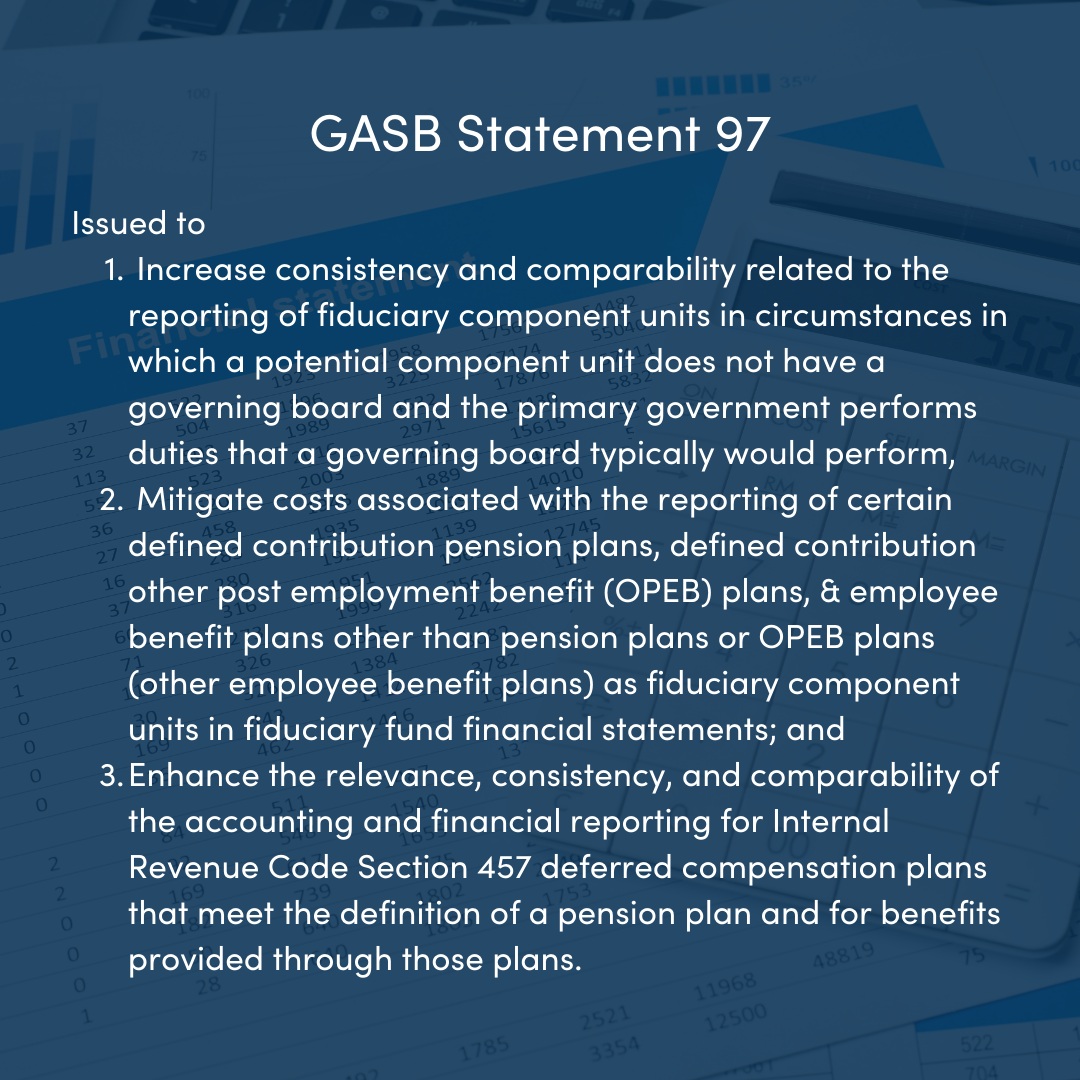

GASB 99

Leases

GASB Statement 87

Accounting for Interest Cost Incurred before the End of a Construction Period

GASB Statement 89

Conduit Debt Obligations

GASB Statement 91

Omnibus 2020

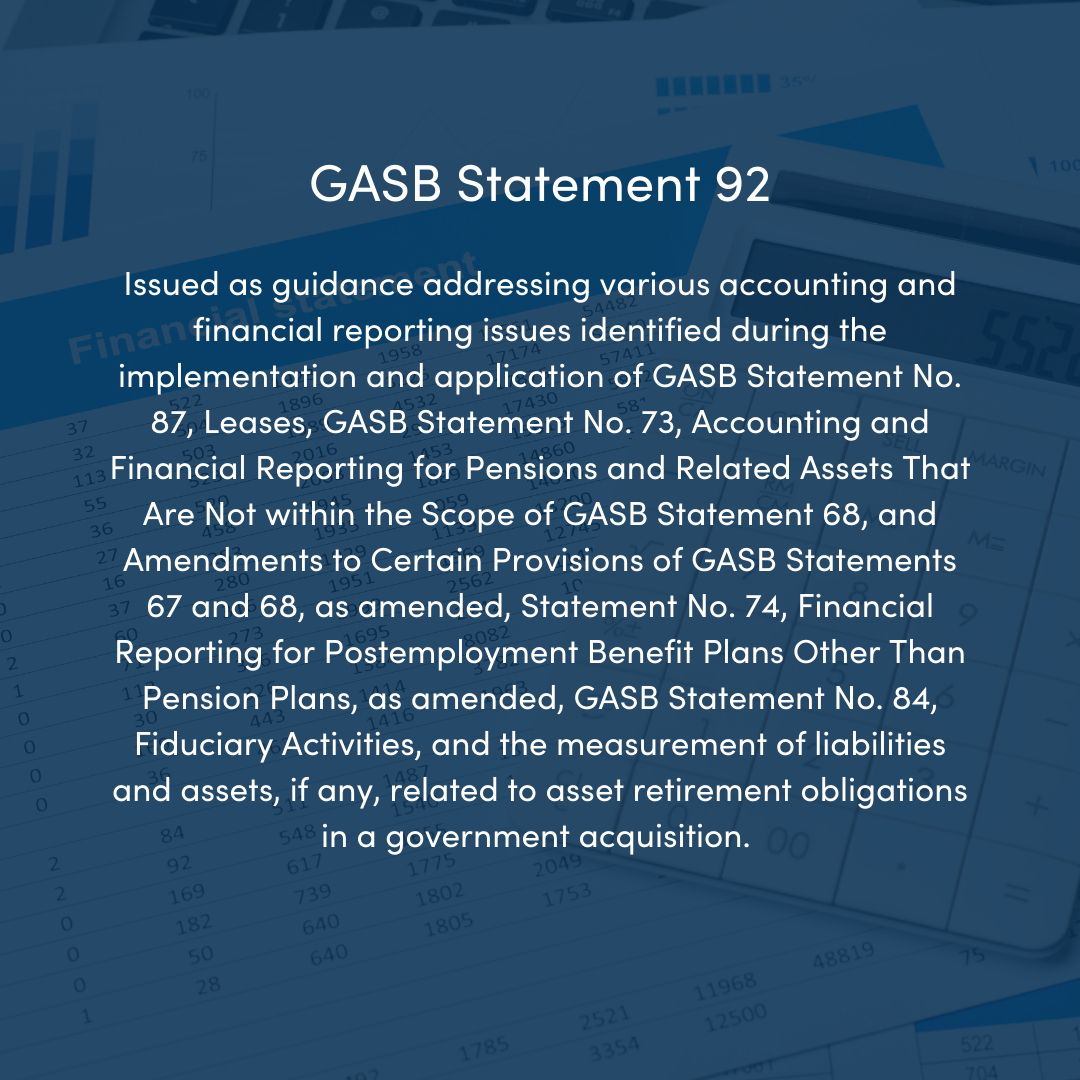

GASB Statement 92

{kind=link}

Replacement of Interbank Offered Rate

GASB Statement 93

{kind=link}

Fiduciary Activities

GASB Statement 84

Majority Equity Interest

GASB Statement 90: An Amendment of GASB Statements No. 14 and No. 61