One Big Beautiful Bill Act

Learn the Changes that Affect You

The One Big Beautiful Bill Act (OBBBA) includes tax reform legislation signed into law by President Trump on July 4, 2025 that primarily focuses on extending and modifying provisions from the 2017 Tax Cuts and Jobs Act (TCJA). It includes a variety of tax changes affecting individuals and businesses, aimed at stimulating economic growth and addressing some of President Trump’s key policy goals. With over 9,000 pages, there is a lot to digest in the OBBBA that can affect Americans financially.

This page serves as a resource for those interested in learning about the updates and how it will affect them. If you are a client and would like to set up a custom planning meeting, our team looks forward to working with you to ensure you’re using the changes to your advantage. Click the button below or call us to set up a meeting.

Business Tax Provisions

Permanently restored: Immediate expensing for domestic research and development (R&D) expenses. Instead of deducting these expenditures over a 5-year period, this provision allows taxpayers to immediately deduct domestic research or experimental expenditures paid or incurred in taxable years beginning after December 31, 2024, and before January 1, 2030.

Small businesses with gross receipts of $31 million or less can retroactively expense R&D back to after December 31, 2021 and all other domestic R&D between December 31, 2021 and January 1, 2025 can accelerate remaining deductions over a one- or two-year period.

Permanently restored: 100% bonus depreciation, which means businesses can immediately deduct the full cost of qualifying tangible property. This applies to eligible assets acquired and placed in service after January 19, 2025.

This includes assets like machinery, equipment, and certain improvements. For real estate, this could involve a cost segregation study to identify and depreciate building components with shorter useful lives. For example, under OBBB, qualified production property (QPP) used for manufacturing, production, or refining of certain tangible personal property in the US is eligible for 100% bonus depreciation through 2030.

Increased: This provision increases the Section 179 expensing limits, allowing businesses to immediately deduct more of the cost of qualifying property:

- New limit: Up to $2.5 million can be expensed.

- Phase-out threshold: Begins phasing out when total qualifying property placed in service exceeds $4 million.

- Both amounts will be adjusted for inflation starting in 2026.

- Applies to property placed in service in tax years beginning after December 31, 2024.

This makes it easier for small and mid-sized businesses to invest in assets without the complexity of long-term depreciation.

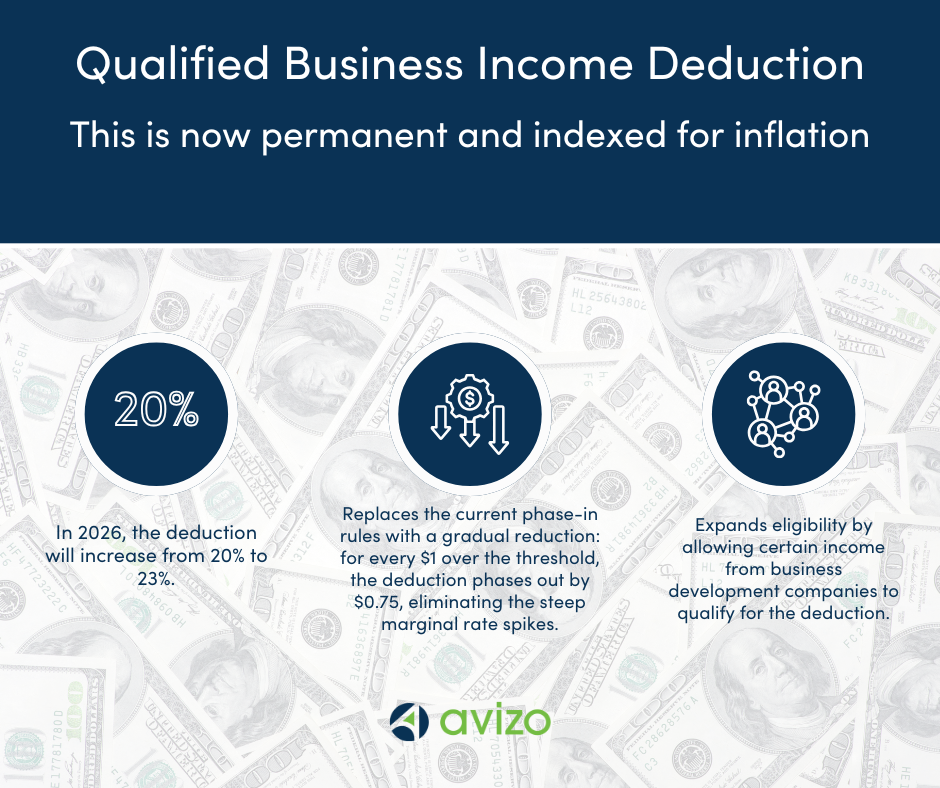

Permanently restored: 199A (QBI) deduction provisions permanent and keeps the deduction rate of 20%.

{kind=link}

This provision also expands the deduction limit phase-in range by increasing the $50,000 (non-joint returns) and $100,000 (joint returns) amounts to $75,000 and $150,000, respectively. This eases the impact of those limits for “specified service trades or businesses” as well as for entities subject to the wage and investment limitations in Code Section 199A. The OBBB also introduces a new, inflation-adjusted, minimum deduction of $400 for taxpayers who have at least $1,000 of QBI from one or more active trades or businesses in which the taxpayer materially participates. These changes, collectively, create a more favorable tax position for some small businesses, by increasing deductions for QBI for those that qualify for these new provisions.

Permanently restored: EBITDA-based limitation on business net interest deductions.

This provision also temporarily increases the cap for tax years 2025–2029 by calculating income using EBITDA instead of EBIT, allowing for greater deductions. It also permanently expands the definition of “motor vehicle” to include certain trailers and campers designed to be towed or attached to a vehicle.

New: Implement a 1% floor on the deduction of charitable contributions made by corporations.

In addition to the annual ceiling of 10% of taxable income that is applied to a corporation’s charitable contributions, the OBBB puts a floor of 1% of taxable income on the amount of charitable contributions a corporation must make to receive a deduction, effective beginning in 2026.

Repealed: There is now accelerated phase outs and eliminations of many of the green energy tax credits enacted as part of the 2022 Inflation Reduction Act.

Expanded: the tax exclusion for gains from the sale of QSBS.

The OBBB includes three significant expansions to Section 1202, the exclusion of gain recognition for the sale of qualified small business stock (QSBS):

- The required holding period for QSBS benefits for stock acquired after the applicable date would be reduced from 5 years to 3 years, with 50% benefits phasing in beginning after a three-year holding period. A four-year holding period rises to 75%, and a five-year holding period receives the full 100% exclusion.

- $15 million (up from $10 million) of gain from stock acquired after the applicable date could be excluded. Note, however, that the 10x basis rule does not change, so the exclusion will apply to the greater of $15 million or 10x the taxpayer’s basis.

- The permitted gross assets limit increases from $50 million to $75 million.

Permanently increases: The employer-provided child care credit (section 45F) is increased from $150,000/year on up to 25% percent of qualified child care expenses provided to employees to $500,000/year on up to 40%.

A business must spend at least $1.25 million on child care related expenses to receive the new full credit.

Makes permanent: Opportunity Zone (OZ) incentives, with some changes.

The most significant is the change to the definition of “low-income community:” The definition of “low-income community” is narrowed to census tracts that have a poverty rate of at least 20 percent or a median family income that does not exceed 70% (formerly 80%) of the area median income. OBBB also provides enhanced benefits for investments in rural OZs.

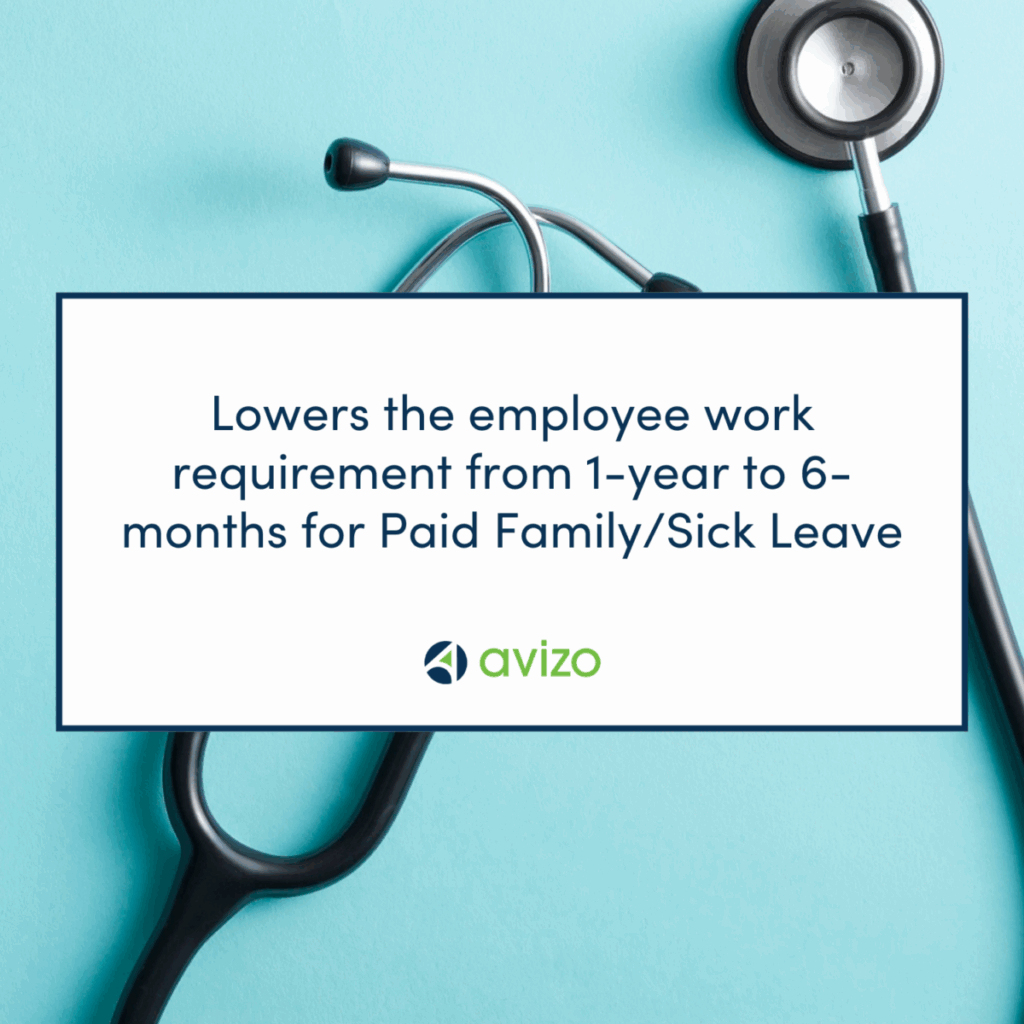

Permanently extends: Code section 45S employer tax credit for paid family and medical leave, originally set to expire at the end of 2025.

This also modifies the credit to be claimed for an applicable percentage of premiums paid or incurred by an eligible employer during a taxable year for insurance policies that provide paid family and medical leave for qualifying employees, and lowers the minimum employee work requirement from 1-year to 6 months at the election of the employer.

Increased Threshold: The OBBB raises the de minimis threshold for information reporting (e.g., Forms 1099-NEC and 1099-MISC), from $600 to $2,000, effective beginning in 2026. This change, although small, may save significant time and effort for businesses that otherwise struggle to meet reporting requirements timely—and who typically file Forms 1099 late (or fail to file them at all).

International Tax Provisions

The international tax provisions maintain the 2017 TCJA changes to GILTI, FDII, and BEAT and proposes new legislation to address “unfair foreign taxes”. Scroll over the icons below to learn more.

GILTI

FDII

BEAT

Enforcement of Remedies Against Unfair Foreign Taxes

Employee Tax Provisions

Temporary Deduction: Up to $25,000 earned as tips can be deducted from income, and this phases out by $100 for each $1,000 of the taxpayer’s modified adjusted gross income that exceeds $150,000 ($300,000 in the case of a joint return).

- You are eligible for both those who itemize and those who use the standard deduction.

- The deduction is allowed for both employees receiving a W-2 and independent contractors receiving a 1099-K or 1099-NEC.

- If the taxpayer is married, the deduction is only available if they and their spouse file a joint return.

- Highly compensated employees are ineligible to receive the deduction.

- A work-eligible Social Security number is required.

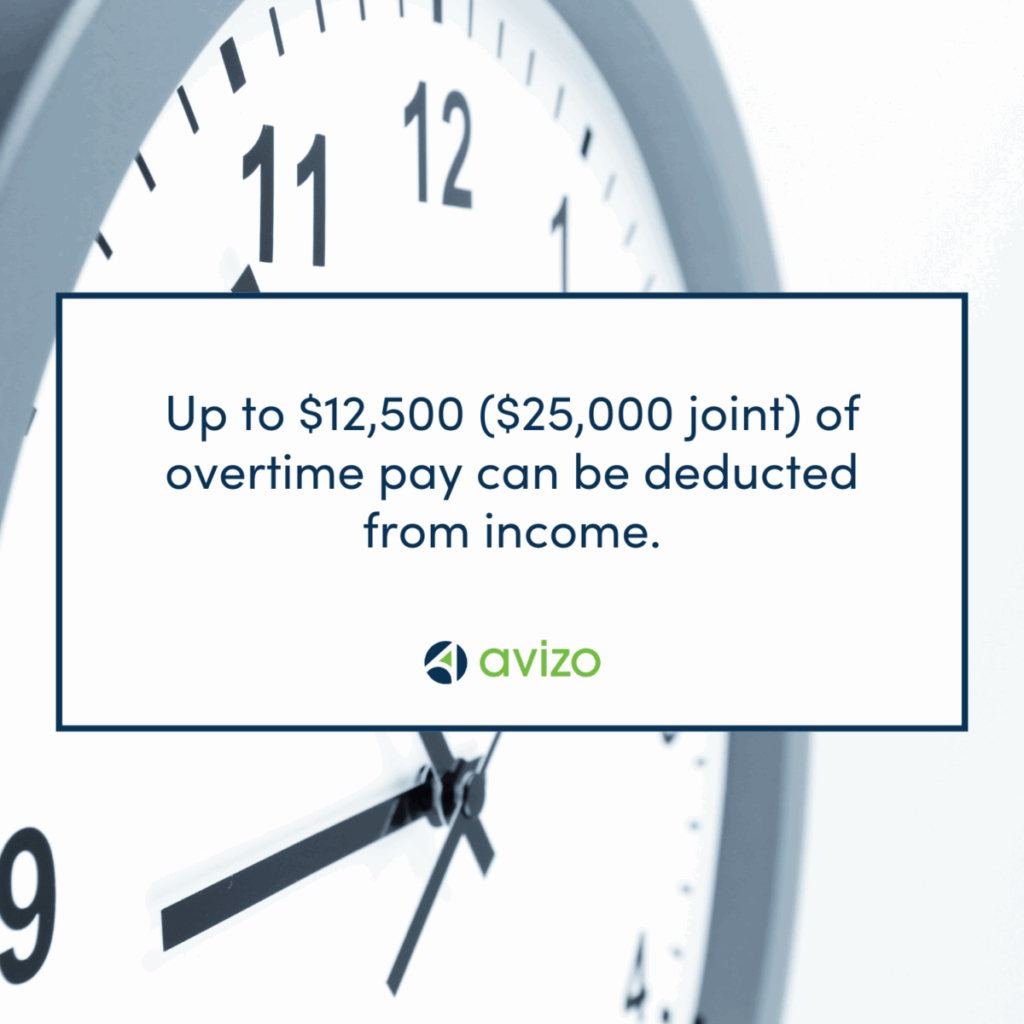

Temporary Deduction: The amount of the deduction may not exceed $12,500 ($25,000 in the case of a joint return). The amount of the deduction is reduced by $100 for each $1,000 of the taxpayer’s modified adjusted gross income that exceeds $150,000 ($300,000 in the case of a joint return).

- You are eligible for both those who itemize and those who use the standard deduction.

- If the taxpayer is married, the deduction is only available if they and their spouse file a joint return.

- Highly compensated employees are ineligible to receive the deduction.

- A work-eligible Social Security number is required in order to claim the deduction.

Increased Eligibility: Although this is a credit for employers, it lowers the minimum employee work requirement from 1-year to 6-months, which expands eligibility for employees.

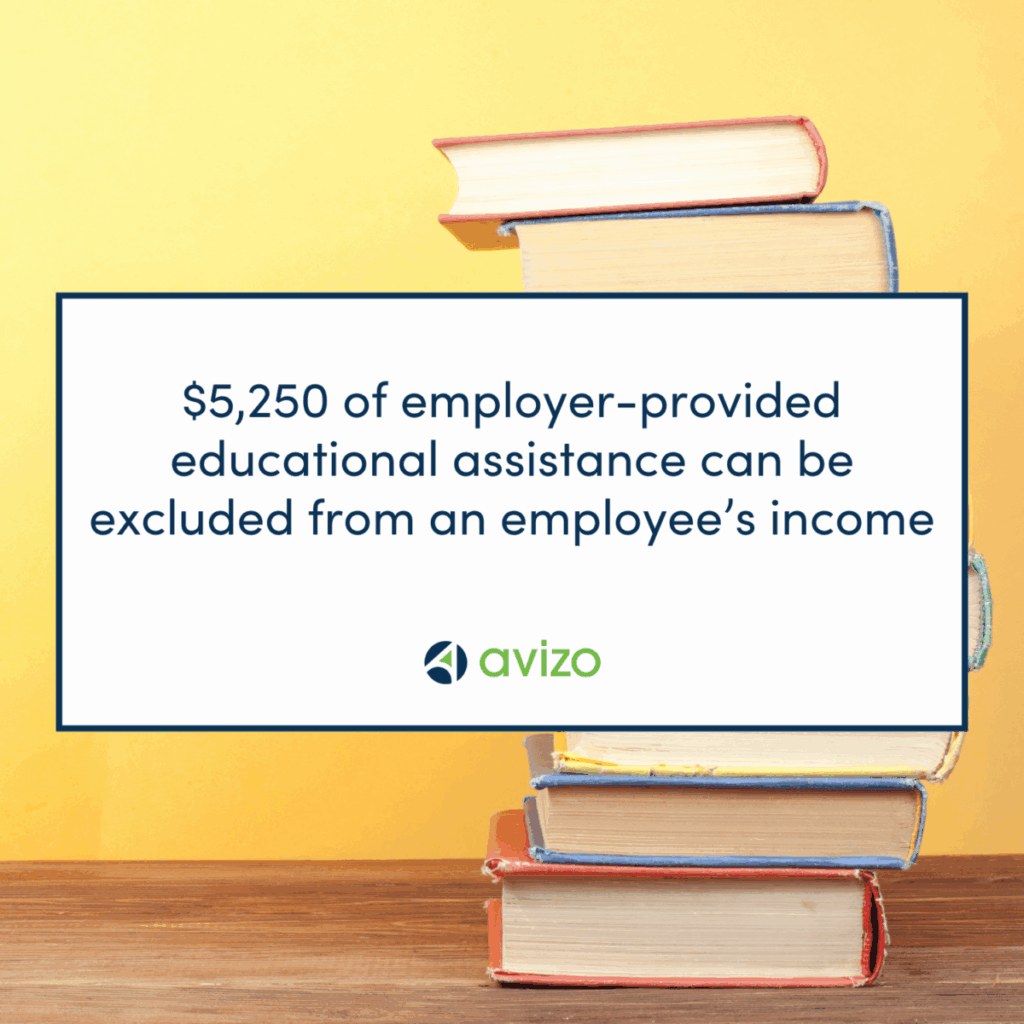

Made Permanent: Permanently allows the first $5,250 of employer-provided educational assistance to be excluded from an employee’s gross income.

Employer-provided education assistance includes the payment, by an employer, of an employee’s educational expenses (including, but not limited to, tuition, fees, and similar payments, books, supplies, and equipment).

Individual Tax Provisions

Made Permanent: The credit of $2,000 per child will be permanent and there will be a temporary increase to $2,500 per child for tax years 2025 – 2028. The income phase-out thresholds are maintained at $200,000 for single filers and $400,000 for joint.

New: The child and parent(s) must have Social Security Numbers (SSN) to get the credit. The parent SSNs must be considered work-eligible.

Made Permanent: Permanently extends the estate and lifetime gift tax exemption and increases the exemption amount to $15 million for single filers; $30 million for married filing jointly in 2026.

This exemption amount is indexed for inflation going forward.

New Deduction: A new charitable income tax deduction is created for non-itemizing taxpayers, allowing deductions of up to $1,000 for single filers and $2,000 for married couples filing jointly.

The charitable contribution must be made to a qualified charity and cannot be made to Donor-Advised Funds or supporting organizations.

Increased: The deduction limit for payment of state and local taxes (the SALT cap) is temporarily increased from the current $10,000 to $40,000. That amount will then be adjusted for inflation, starting with $40,400 in 2026 and increased by 1% annually through 2029. In 2030, the deduction limit reverts to $10,000. However, the amount of the available deduction does phase down for taxpayers with a modified AGI of over $500,000, adjusted annually for inflation with a floor of $10,000.

Temporary Deduction: A $6,000 “bonus” deduction is available for those over 65 with modified gross adjusted income (MAGI) of up to $75,000 for an individual filer and $150,000 for those filing jointly. Each spouse can take the deduction, for a total of $12,000, if both are 65-plus.

- The deduction is reduced for higher earners, and phases out entirely for a single filer earning $175,000 and a couple earning $250,000.

- This applies for the 2025-2028 tax years and is not available after 2028.

New Deduction: Creates an above-the-line deduction of up to $10,000 for qualified passenger vehicle loan interest during a given taxable year.

- Eligibility is tied to income with the deduction decreasing by $200 for every $1,000 of additional income once you hit the following thresholds: $100,000 as a individual or $200,000 as filing joint. (So for example, if you are a single filer earning $120,000, you can only deduct $6,000 of car loan interest.)

- The vehicle must have undergone final assembly at a U.S. factory.

- Elementary, Secondary, Religious Schools: The allowable qualified educational expense for tuition at an elementary or secondary private, public, or religious school is increased from $10,000 to $20,000. Certain non-tuition expenses (e.g., books, online materials, tutoring fees) can now be considered a qualified educational expense.

- Higher Education: For higher education, this provision allows tax-exempt distributions from 529 savings plans to be used for additional qualified higher education expenses, including “qualified postsecondary credentialing expenses” in connection with “recognized postsecondary credential programs” and “recognized postsecondary credentials”.

Made Permanent: Permanently allows the additional contributions to Achieving a Better Life Experience (ABLE) accounts.

- Allows designated beneficiaries who make qualified contributions to their ABLE account to qualify for the Saver’s Credit.

- Allows tax-free rollovers of amounts in Section 529 qualified tuition programs to qualified ABLE programs.

- Modifies the inflation-adjustment base used to calculate the maximum annual contribution to an ABLE account. This would have the effect of increasing the contribution limit (currently $19,000).

- High Deductible Health Plan: An individual may only contribute to an HSA if their sole health insurance coverage is through a high-deductible health plan (HDHP). OBBB will now treat bronze-level and catastrophic plans purchased in the individual marketplace under the Affordable Care Act as HDHPs for purposes of making HSA contributions.

- Direct Primary Care: Individuals participating in direct primary care arrangements can contribute to an HSA. For purposes of this provision, a direct primary care arrangement is an arrangement that solely offers primary medical care provided by a primary care provider. Fees for the services must be fixed periodic fees that cannot exceed $150 ($300 if the arrangement covers more than one individual). Primary care services would not include procedures requiring general anesthesia, prescription drugs, and certain laboratory services.

- Telehealth: An HDHP can provide for telehealth and similar remote-care services without a deductible.

Permanently Eliminated:

- Bicycle Commuting Deduction

- Moving Expenses Deduction (exception for military)

- Miscellaneous deductions

Makes Permanent: The qualified residence interest deduction to is permanently limited to the first $750,000 in home mortgage acquisition debt. It also makes permanent the exclusion of interest on home-equity indebtedness from the definition of qualified residence interest. The bill also treats certain mortgage insurance premiums on acquisition indebtedness as qualified residence interest.

Expanded: Itemized deductions for personal casualty losses now applies to federally declared disasters and certain state-declared disasters.

Decreased Deduction: Defines “losses from gambling” to include any related deductions that would normally be allowed under tax rules. However, the bill limits these gambling losses to 90% of the actual losses. Also, you can only deduct gambling losses up to the amount you won from gambling during the year.

Modified Tax Rates & Brackets

The most substantial change that will affect all taxpayers is the tax brackets and standard deduction rates. These were altered in the 2017 TCJA and are now permanent, with the standard deduction amounts continuing to be adjusted annually for inflation after 2025. Scroll over the icons below to learn more.

Tax Bracket

Adds an additional year of inflation adjustment to all brackets except for the top bracket (37%).

Standard Deduction

For tax years 2025 through 2028, the standard deduction increases by an additional $1,000 for a single filer, $1,500 for head of household, and $2,000 for married filing jointly.

Personal Exemptions

Set up a Meeting

Any time there are substantial changes to tax law, it is important to set up a meeting with your financial and tax advisors. We can help guide you to making decisions that will generate the most positive impact for your business and personal goals. If you want to learn more about how to take advantage of these changes for your personal situation, let’s set up a meeting this summer to get you ready for 2026 and beyond.