The Financial Accounting Standards Board (FASB) issued Accounting Standards Update (ASU) 2020-07, Presentation and Disclosures by Not-for-Profit Entities for Contributed Nonfinancial Assets in September 2020, which will change the reporting requirements for in-kind donations. These nonfinancial assets may include tangible goods such as clothing, food, vehicles, and supplies/materials, but also contributed services such as accounting, legal, or other specialized volunteer services.

Why is this Changing?

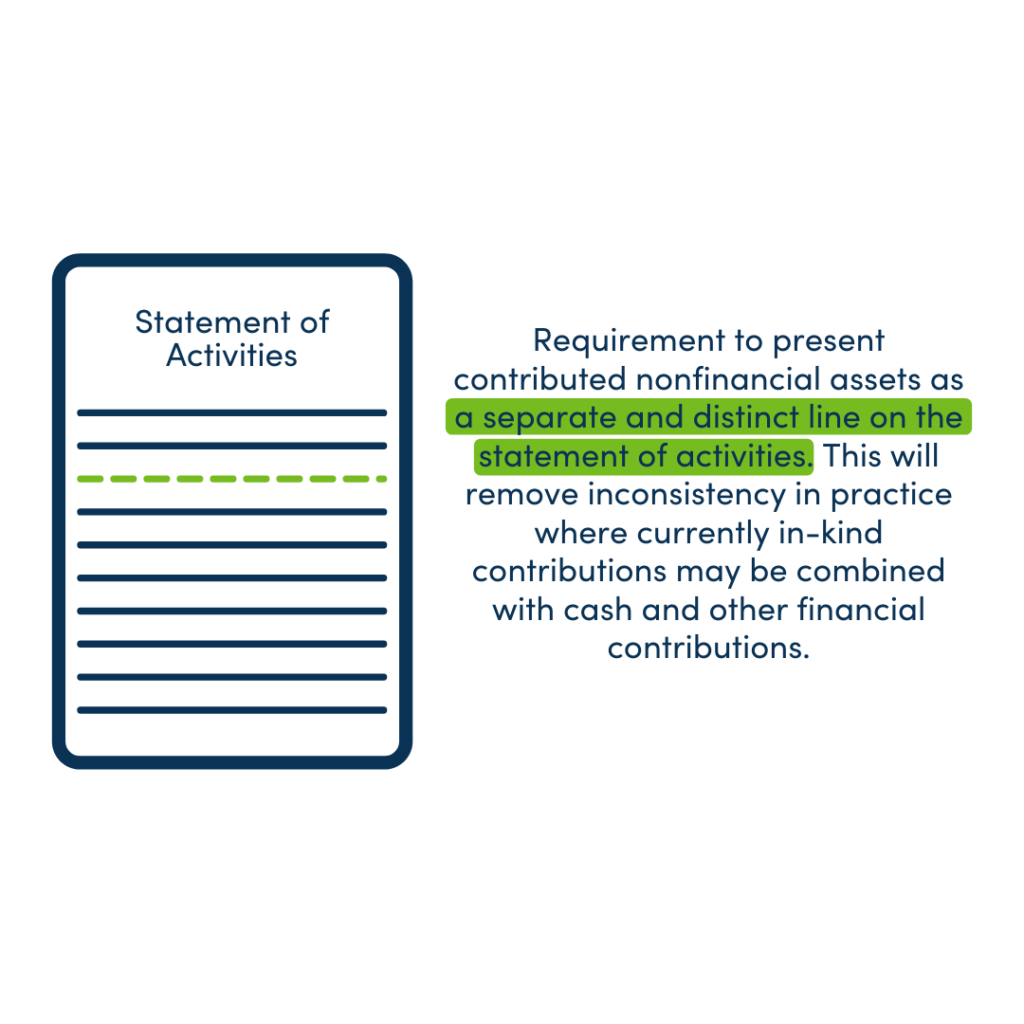

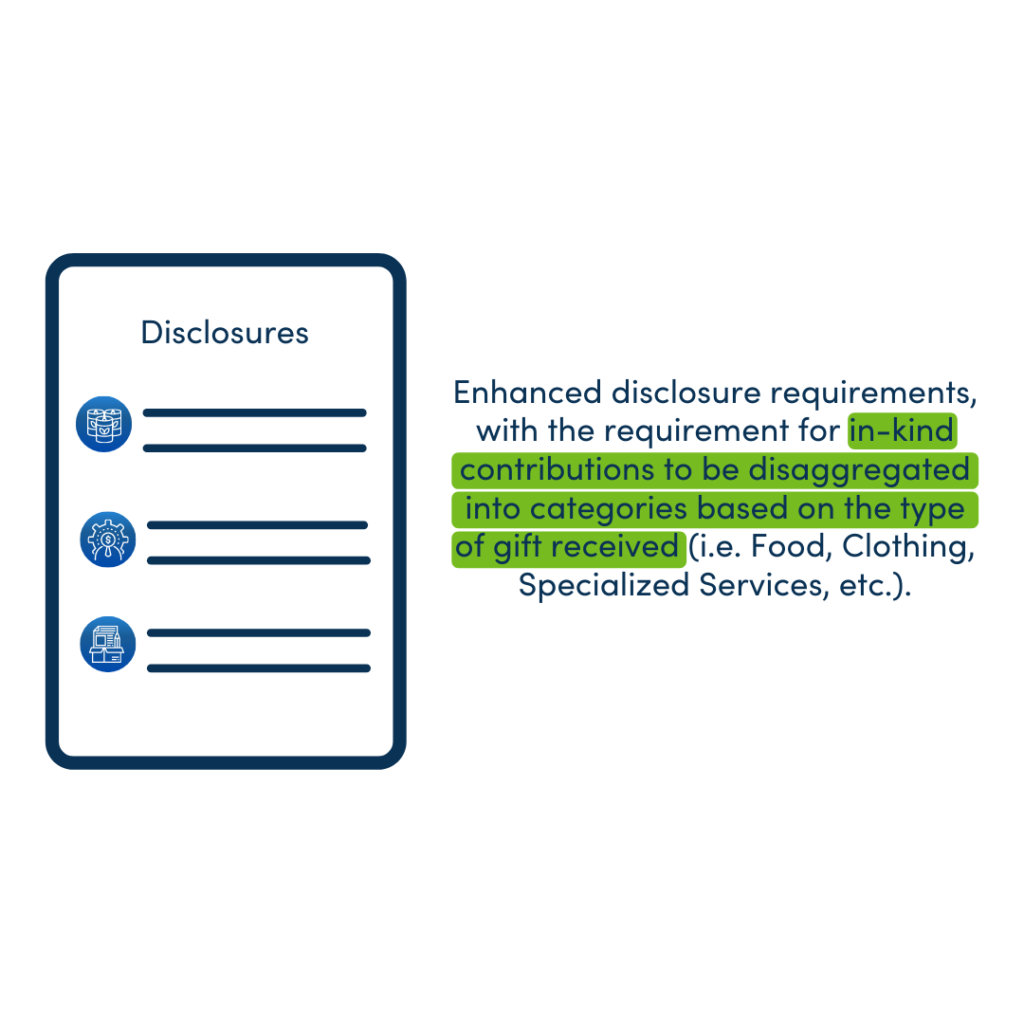

The COVID-19 pandemic resulted in major operational changes for nonprofit organizations. Many actually experienced an increase in the amount of in-kind contributions they received and the Accounting Standards Update (ASU) is designed to increase transparency and consistency in the reporting of these items. Here are the two major provisions:

The ASU also requires disclosure for each disaggregated category of in-kind contributions, including:

- A description of any donor-imposed restrictions associated with the in-kind contribution.

- The organization’s policy about monetizing rather than utilizing in-kind contributions.

- Qualitative information about whether the in-kind contributions were either monetized or utilized during the reporting period. If utilized, a description of the programs or other activities in which those in-kind contributions were used is required.

- A description of the valuation techniques and inputs used to arrive at a fair value measurement.

- The principal market (or most advantageous market) used to arrive at a fair value measurement if it is a market in which the organization is prohibited by a donor-imposed restriction from selling or using the contributed nonfinancial assets.

When Do We Start?

The ASU is required to be applied to annual reporting periods beginning after June 15, 2021 (the fiscal year ends June 30, 2022 and later). However, the ASU is required to be applied retrospectively, which means comparative information for all presented fiscal years (typically 2021 fiscal year ends) will be necessary. Leaders of not-for-profit organizations need to start gathering the information necessary for the application of this standard.

We can help you with the determination of the categories of disaggregation and the potential adoption of a policy to monetize or use certain in-kind contributions, among other items. Just contact us at [email protected]!